What Happens If I Return a Car to the Lender Before Payoff?

Table of Contents

What Happens If I Return a Car to the Lender Before Payoff?

Quick overview of what happens next

What is a “voluntary repossession” in plain English?

A voluntary repossession is when you tell the lender you can’t keep the car and you return it instead of waiting for them to take it. Experian describes it as arranging the surrender directly with the lender.

It can be less chaotic than an involuntary repossession. You usually have more control over timing and you can remove your personal items first. It’s still a repossession event in the lender’s system, and the financial math works similarly either way.

Does returning the car cancel the loan?

No, returning the car usually does not cancel the loan.

Tennessee’s Attorney General explains that the sale proceeds go toward the balance and the costs of the sale and repossession. If the proceeds don’t cover what you owe and the expenses, the creditor may pursue you for the amount owed, including certain fees.

That remaining amount is commonly called a deficiency balance. This is the biggest surprise for most borrowers.

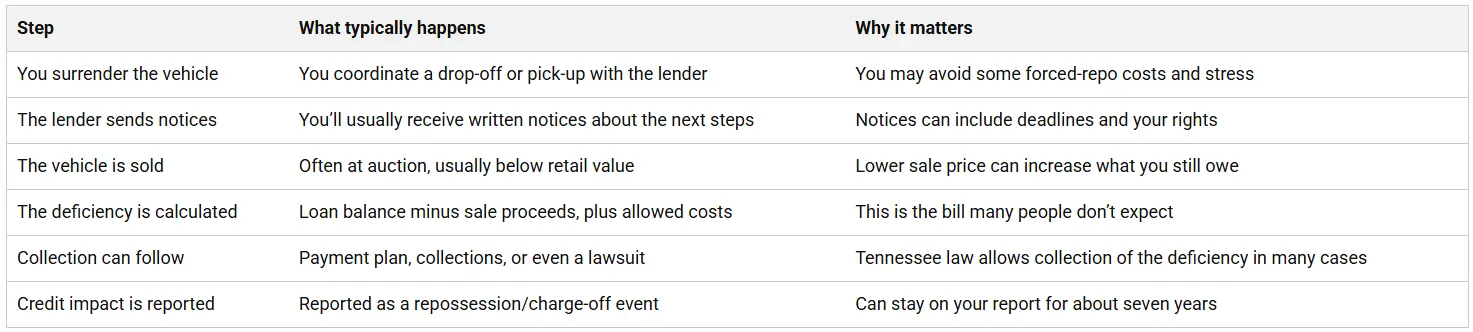

What happens after I return the car to the lender?

Most borrowers experience a version of the same timeline. Your contract can change the details, but the steps below are common.

- You contact the lender and arrange surrender.

- Get the drop-off time, location, and required items in writing if possible.

- The lender takes possession and prepares the vehicle for sale.

- They may add costs tied to storage, transport, or sale prep depending on the situation.

- You receive notices about the sale or the lender’s plan.

- Tennessee resources note you may have rights related to notice and redemption, depending on the terms and timing.

- The vehicle is sold, often at auction.

- Auction prices are typically lower than retail, which is why deficiencies are common.

- The lender calculates what you still owe and sends an accounting.

- This is where your deficiency balance shows up, along with itemized costs in many cases.

- Collections may begin if the deficiency isn’t resolved.

- Tennessee’s Attorney General notes creditors may sue for the amount owed and certain costs when proceeds don’t cover the balance and expenses.

What is a deficiency balance, and how is it calculated?

A deficiency balance is the amount left over after the lender sells the car and applies the sale proceeds to your loan. Costs tied to repossession and sale can also be added, depending on your agreement and what’s allowed.

Here’s a simple example:

- Loan payoff amount at surrender: $15,000

- Auction sale price: $9,000

- Sale/repo-related costs added: $800

- Estimated deficiency balance: $6,800

Even if you returned the car peacefully, the math can still leave a sizable bill. That’s why it’s smart to look at alternatives first.

What fees can still be charged after a voluntary surrender?

Even with a voluntary surrender, fees can show up. Tennessee’s Attorney General specifically notes repossession fees, auction costs, and legal fees may be pursued if sale proceeds don’t cover the loan and expenses.

Voluntary surrender can reduce some costs compared with an involuntary repossession, especially towing or storage fees in certain situations. Sources like NerdWallet and Experian note potential cost and stress advantages when you coordinate proactively.

How will a voluntary repossession affect my credit?

A voluntary repossession can significantly damage your credit. It may also be paired with late payments leading up to the surrender, which compounds the hit.

Repossession-related negative items can generally remain on your credit report for around seven years, often counted from the first delinquency that led to the repossession.

If you’re asking, “Will lenders treat voluntary repossession differently than involuntary?” the honest answer is: sometimes a little, but not enough to make it painless. Some lenders may view proactive communication more favorably, but you should still expect tougher approvals and higher rates for a while.

Is voluntary repossession better than waiting for the lender to take the car?

It can be better in a narrow sense, but it’s rarely “good.”

Voluntary surrender can help you control the timing, avoid the surprise of a forced repo, and potentially reduce some extra fees tied to retrieval.

But both paths can still lead to a deficiency balance and long-lasting credit damage. If you have any workable alternative, it’s usually worth exploring first.

What happens to my personal items if I return the car?

With a voluntary surrender, you can remove your belongings before you turn in the vehicle. That’s one of the practical advantages of doing it on your terms.

Before you hand it over, check every compartment: glove box, console, door pockets, trunk, under-seat areas, and any aftermarket storage. Also, remove toll tags, garage remotes, and any personal paperwork. Take photos of the interior and exterior so you have a record of the condition at surrender.

Can the lender sue me after I return the car?

If you have a deficiency balance and don’t resolve it, legal action is possible. Tennessee’s Attorney General notes that when sale proceeds don’t cover the loan and expenses, the creditor may sue for the amount owed, including certain fees.

If you’re at this stage, it’s smart to ask about a written settlement offer or structured payment plan before it escalates. You can also consider talking to a qualified attorney or a nonprofit credit counselor for guidance specific to your situation.

Alternatives to returning the car before payoff

If you’re trying to lower your monthly payment or get out of an upside-down loan, there are usually better options than surrendering first. These are the most common “least-damage” moves borrowers consider.

In Morristown, private-party demand for reliable commuter vehicles and AWD SUVs can be strong in-season, which can help you get closer to your payoff than an auction would. Selling yourself takes more work, but it often saves real money.

When does voluntary repossession actually make sense?

Voluntary repossession can make sense when you’ve exhausted other options, and the payment is truly unworkable. It may also be the last step before the account falls further behind, especially if you’re trying to reduce late fees and stop the situation from spiraling.

If you’re considering it, focus on damage control. Ask the lender what fees will be added, how the sale will be handled, and how quickly you’ll receive the post-sale statement. Get as much as you can in writing.

A simple checklist before you surrender a vehicle

Next Steps: Explore Your Options With Farris Motor Company

Farris Motor Company can help you explore affordable options if you’re trying to reset your payment and move forward. View our current selection here: Farris Motor Company Inventory, and start your financing steps here: Farris Motor Company Credit Application.

Frequently Asked Questions

What happens if I voluntarily surrender my car in Tennessee?

In most cases, the lender sells the vehicle and applies the proceeds to your balance. If the sale doesn’t cover what you owe plus allowed expenses, you may still owe a deficiency balance, and the creditor may pursue collection.

Will I still owe money after returning the car to the lender?

Often, yes. Because vehicles frequently sell at auction for less than the payoff amount, many borrowers end up with a deficiency balance after surrender.

How long does a repossession stay on my credit report?

Repossession-related negative credit information commonly remains for around seven years, often measured from the first missed payment that led to the repossession.

Is a voluntary repossession better for my credit than an involuntary repossession?

It may look slightly better in the sense that you communicated and cooperated, but it can still be reported as a repossession and cause serious credit damage.

Can I get my car back after repossession or surrender?

Tennessee consumer resources note that you may have a right to redeem the vehicle up until it is sold or within certain notice timelines, depending on the situation and agreement terms.

What should I do before I decide to return the car?

Start by calling your lender and asking about hardship options, reinstatement, and the full cost breakdown of surrender. If selling privately or refinancing is possible, those routes often reduce long-term damage compared with surrendering first.