How Do I Trade In My Car With an Upside-Down Loan in Jefferson City or Morristown, TN?

How Do I Trade In My Car With an Upside-Down Loan in Jefferson City or Morristown, TN?

You can trade in a car with an upside-down loan by paying the difference, rolling the negative equity into a new loan, structuring your next deal to minimize the rollover, or waiting until you owe less than the car is worth.

If you’re shopping at Farris Motor Company in Jefferson City or Morristown, you’re not the first person to feel stuck by negative equity. The good news is that trading in with an existing lien is common, and there are several smart ways to do it without creating a bigger problem on your next vehicle.

This guide walks through the numbers you need, the options that work best in real life, and what to watch for in the paperwork.

The 5-step trade-in plan

- Get your current payoff amount from your lender.

- Get a real trade-in appraisal (not just an online estimate).

- Calculate your negative equity (payoff minus trade value).

- Choose a strategy: pay it, roll it carefully, reduce it with a deal structure, or wait.

- Pick a vehicle and loan term that helps you build equity faster, not slower.

What does it mean to be upside down on a car loan?

Being upside down (negative equity) means your loan payoff is higher than your vehicle’s trade-in value.

Example:

- Your car’s trade-in value: $10,000

- Your loan payoff: $13,500

- Negative equity: $3,500

That $3,500 doesn’t disappear when you trade. It either gets paid now (cash/down payment) or gets added into the next loan (rollover).

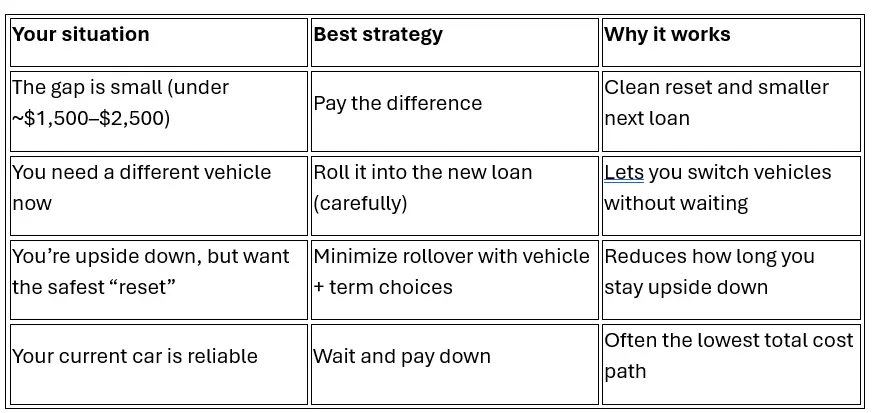

Which option fits your situation?

Step 1: Get your payoff amount and your real trade-in value

Get your payoff amount (not just your balance)

Call your lender and ask for a payoff quote. Payoff can be different from your current balance because interest accrues daily, and fees may apply.

Get a real appraisal

Online values are a helpful starting point, but a store appraisal reflects actual local market demand and your specific vehicle condition.

Farris Motor Company offers trade/sell tools and can help you start the process online, then confirm value in person at either location.

Step 2: Calculate your negative equity (this number drives everything)

Use this simple formula:

Loan payoff − trade-in value = negative equity

Once you know the number, the “best option” usually becomes obvious. Most bad trade-in outcomes happen when people skip this step and shop based on monthly payment only.

Step 3: Choose how you’ll handle the negative equity

Option A: Pay the difference out of pocket

If you can cover the negative equity (or most of it), this is usually the cleanest approach. It lowers the amount financed on the next loan and can help you get back to positive equity faster.

This option is especially helpful if you’re trying to keep your next payment stable.

Option B: Roll the negative equity into the new loan

This is common, and it can be the right move when your current vehicle no longer fits your needs.

The FTC warns that “we’ll pay off your loan no matter what” ads can be misleading if the negative equity is simply added to the next loan (or taken out of your down payment). You want to see exactly where it shows up in the contract.

If you roll negative equity, focus on keeping the next deal tight: reasonable vehicle price, realistic term, and minimal extras added to the amount financed.

Option C: Minimize the rollover with smarter deal structure

If you’re upside down but you want to avoid staying upside down for years, this is the strategy.

Here’s what “minimize rollover” usually means:

- Choose a vehicle price that fits your budget (don’t “upgrade” into a bigger loan).

- Use a down payment to shrink the amount that gets rolled in.

- Choose the shortest term you can comfortably afford. Longer terms can keep you upside down longer.

This approach is often the best mix of “I need a new vehicle now” and “I don’t want to repeat this problem.”

Option D: Wait and pay down the balance

If your current vehicle is still dependable, waiting can be a strong financial move. Each payment reduces the payoff, and you may reach break-even sooner than you think.

This is also a good time to check refinancing options, because a lower rate can help you pay down principal faster.

Step 4: What happens to the lien and payoff in Tennessee?

When you trade in a vehicle you’re still financing, the lien has to be satisfied as part of the process. In Tennessee, lien discharge paperwork requirements are handled through the Tennessee Department of Revenue’s title and registration processes.

Tennessee law also addresses dealer responsibilities around liens and title in certain situations. For example, state legislation has language requiring dealers to satisfy liens and obtain title within 30 days of accepting a transfer in specified circumstances.

In addition, Tennessee legislation includes language tied to motor vehicle transactions and trade-in indebtedness that references paying off agreed indebtedness within 30 days after the dealer receives funding from the financial institution on the financing contract.

Practical tip: keep making your normal payments until you have confirmation your lender received and processed the payoff, so you avoid late fees or credit reporting issues during the transition.

Step 5: Choose the right vehicle so you don’t end up upside down again

If you’ve ever wondered, “Why do I keep getting upside down?” the answer is usually a mix of depreciation and long loan structure. Edmunds and Experian both note that rolling negative equity into the next loan can raise costs and can put your next loan upside down immediately, especially if you stretch the term.

When you’re rebuilding equity, these are usually the safest moves:

- Keep the vehicle price reasonable for your budget

- Avoid very long terms if you can

- Put something down (even a modest amount helps)

- Choose models with strong long-term demand in East Tennessee

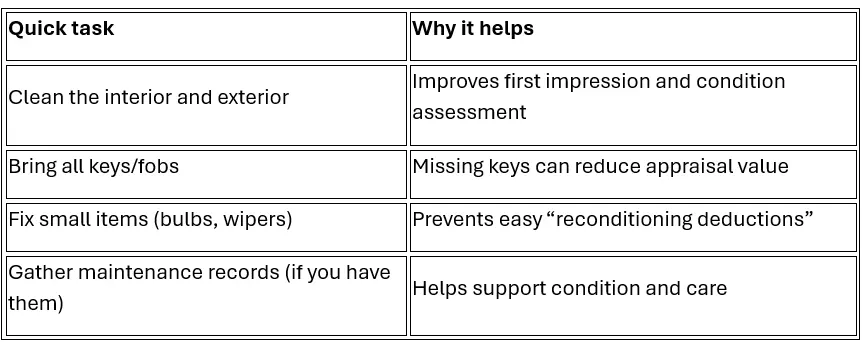

Trade-in prep checklist: how to get the most for your car

A higher trade value reduces how much negative equity you have to deal with.

Should I consider GAP if I’m rolling negative equity?

Many buyers ask this for a good reason. If your loan balance is higher than the vehicle value, a total loss can leave you owing money after insurance pays.

The CFPB explains that Guaranteed Asset Protection (GAP) is optional and is intended to cover the difference between what you owe and what your insurance company pays if the car is stolen or totaled.

GAP isn’t a fit for every situation, but it’s worth discussing if your amount financed is high compared to the vehicle value.

Why shoppers in East Tennessee work with Farris Motor Company

Farris Motor Company has two full-service locations in Jefferson City and Morristown, serving communities from Jefferson County and northern Knox County to Hamblen County and the Cherokee Lake area.

They also make it easy to start online with trade-in tools and online credit approval, then finalize details in-store.

If you’re upside down, the biggest win is getting a clear plan and clear numbers before you commit to the next loan.

Visit Farris Motor Company in Jefferson City or Morristown

Farris Motor Company’s Jefferson City location is at 246 E. Broadway Blvd., Jefferson City, TN 37760.

Farris Jeep in Morristown is at 910 W Morris Blvd, Morristown, TN 37813.

If you want, bring your payoff info and let the team walk you through what your trade is worth, what the negative equity looks like, and which path fits your budget best. Get pre-approved and check out our inventory today!

Frequently Asked Questions About Trading In a Car With an Upside-Down Loan in Jefferson City and Morristown, TN

Can I trade in my car if I still owe money on it?

Yes. You can trade in a financed car, but the payoff amount and any negative equity must be addressed in the deal structure.

Is rolling negative equity into a new loan a bad idea?

Not always, but it usually increases the amount financed and can keep you upside down longer, especially with a long-term loan.

How do I find out exactly how upside down I am?

Get your payoff quote from your lender and subtract your trade-in value from that payoff. The difference is your negative equity.

Will the dealer “pay off my loan no matter what”?

Be cautious with that phrase. The FTC warns that the negative equity may be rolled into the new loan or taken from your down payment, so you want to see it clearly in writing.

How long should it take for a trade-in loan payoff to happen in Tennessee?

Timing depends on funding and processing, but Tennessee legislation includes 30-day requirements tied to satisfying liens/title in certain dealer transfer situations and language referencing payoff of agreed trade-in indebtedness within 30 days after the dealer receives funding.